Funding

The report reveals a decline in investor interest in startups. Globally, venture capital funding dropped by 18% in Q2 2023, reaching USD 65 billion, and the first half of the year saw a 51% decline compared to 2022. The AI sector contributed significantly to the total funding, preventing a more severe downturn. In Poland, the second quarter of 2023 saw 116 companies raising PLN 429 million from 69 funds, marking a 70% YoY decline over six months. The report indicates a slowdown in the startup ecosystem amid reduced investor enthusiasm.

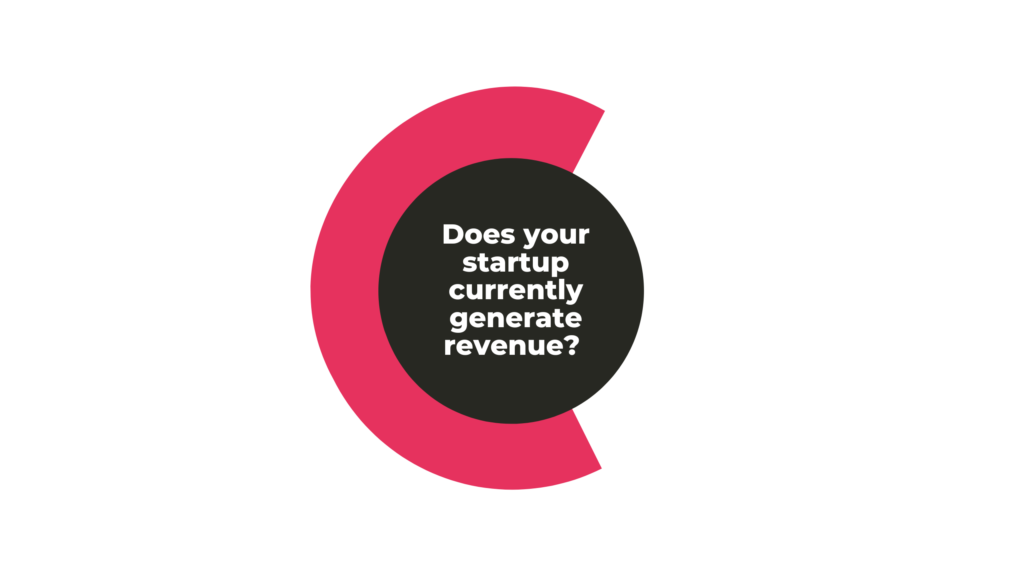

In the recent survey, 65% of startups reported generating revenue, indicating a relatively stable financial situation for most Polish technology companies. Despite the challenging capital market, over half (51%) of startups reported significantly higher revenues than the previous year, with 26% experiencing slight improvements. Only 7% noted a slight deterioration, and 4% expressed more pronounced concerns. Monitoring how the market’s challenges impact startup revenues will be crucial in the coming months.

The Revenue Models

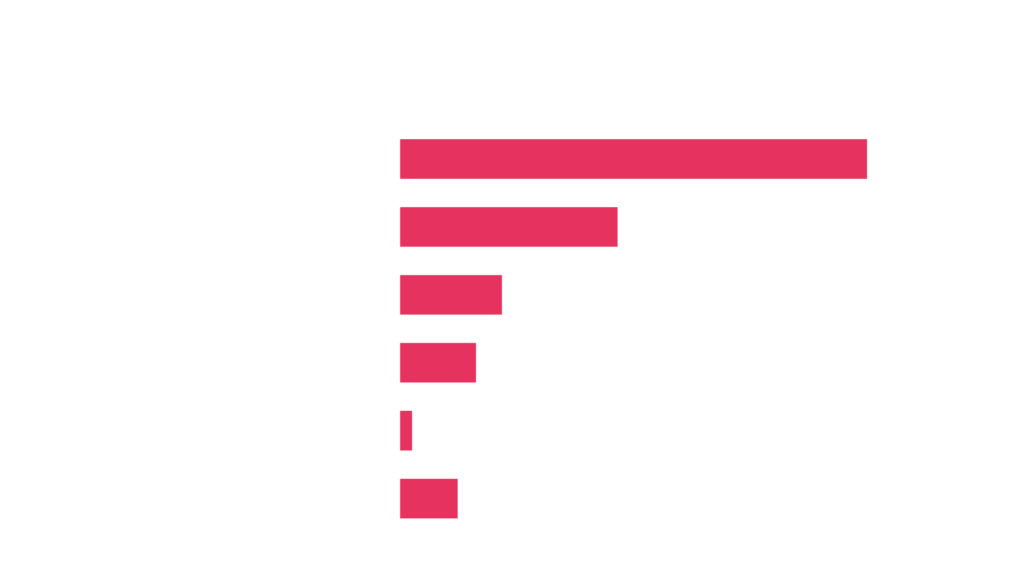

The majority of startups (73%) generate revenue through sales, such as content, advertising, products, or services. Additionally, 34% operate through licensing, involving technology or product usage rights. Other revenue models include business-to-business (B2B) intermediation (16%) and profit-sharing (12%). A small percentage (9%) of startups have not established their own revenue model yet.

The majority of startups (76%) initially rely on bootstrapping, utilizing the founders’ personal savings, before seeking external funding. Among external funding sources, domestic venture capital (VC) funds are the most common, with 25% of respondents benefiting from their support. Foreign VC funds supported 8% of the startups. Business angels are also mentioned, with 24% receiving support from domestic ones and 7% from foreign ones.

State-owned entities, particularly the National Centre for Research and Development (23%), PARP (Polish Agency for Enterprise Development) (16%), and PFR (Polish Development Fund) (8%), play a significant role in providing funding for Polish startups. Domestic accelerators are also notable, with 21% of startups benefiting from them, while foreign accelerators supported 9%. Revenue-based financing was utilized by 5% of respondents. Other sources, like bank loans (6%), industry investors (5%), university incubators (5%), local government programs (4%), crowdfunding (4%), stock market, venture debt, and other niche options, play a smaller role.

Among startups with external funding, 26% have completed only one funding round, 10% have gone through two rounds, and 6% have experienced three rounds. Entities with four or more rounds constitute 2% of the surveyed startups.

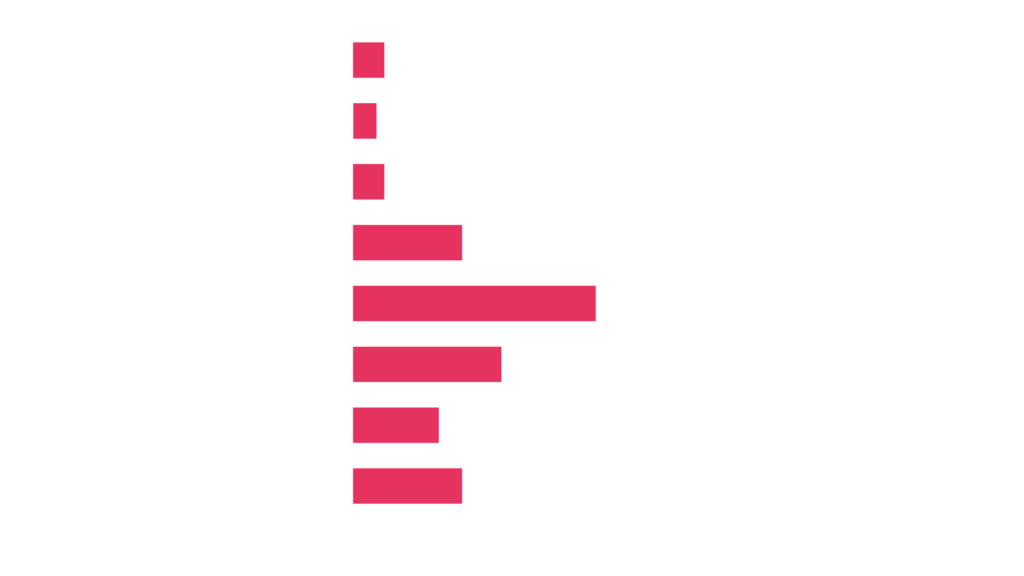

In terms of the amounts raised in all funding rounds, 31% of startups secured between PLN 1 and 2 million, 19% raised PLN 2-5 million, and 11% secured between PLN 5 and 10 million. Those with more than PLN 10 million constitute 14% of respondents. On the lower end, 14% raised between PLN 500,000 and 1 million, 4% secured between PLN 300,000 and 500,000, and 7% obtained a maximum of PLN 300,000 in previous rounds.

What Does it Mean for The Lesser Poland Region

- Technology Focus: The report emphasizes the importance of technological advancements for economic resilience, with one-third of Polish startups prioritizing keywords like AI, deeptech, and IoT. In Lesser Poland, startups can leverage this trend by aligning their focus on these technologies to stay competitive and attract investors.

- Regional Presence: While Mazovia and Lower Silesia are identified as the most active regions for startups, Lesser Poland also shows a significant presence. The region can capitalize on its strengths and unique offerings to further develop its startup ecosystem and attract talent and investment.

- Revenue Growth: The positive outlook on revenue growth in the startup sector, with 51% reporting better revenues than the previous year, indicates a potential for economic stability. Startups in Lesser Poland can use this trend to their advantage, showcasing their growth and attracting investment.

- Funding Challenges: The report highlights a decline in investor interest globally, impacting Poland as well. Startups in Lesser Poland may face challenges in securing funding, and efforts should be directed towards effective fundraising strategies, possibly leveraging regional and national funding sources.

- Industry Specializations: The emphasis on industries like foodtech, cleantech, and medtech suggests areas of potential growth. Startups in Lesser Poland can explore opportunities in these sectors, aligning their innovations with national and global trends.

- Founder Profiles: The profile of startup founders, predominantly older and with prior work experience, challenges stereotypes. In Lesser Poland, initiatives can be undertaken to encourage individuals with diverse backgrounds and experiences to venture into entrepreneurship.

- Human Resources and Well-being: The focus on staff competences and well-being is crucial. Startups in Lesser Poland should prioritize employee development and well-being initiatives to attract and retain talent, especially given the challenges in the global job market.

- Regional Funding Sources: The involvement of state-owned entities like the National Centre for Research and Development in funding startups suggests that regional startups can explore such local funding options. Engaging with regional accelerators and incubators may also provide valuable support.

- Revenue Models: Understanding the prevalent revenue models, with sales being the primary source for 73% of startups, can guide startups in Lesser Poland in designing effective business models that align with market preferences.

- Challenges and Opportunities: Identifying barriers such as the cost of hiring employees and funding acquisition, as well as seeking support in various areas, provides a roadmap for startups to address challenges. Lesser Poland startups can strategize to overcome these hurdles by taking note of local and global trends/patterns, and by anticipating, instead of reacting to them.